U2.16 — Purpose and Features of Key Financial Reports

Overview

Dotpoint 16: purpose and features of key financial reports.

Financial reports help a business record, organise and understand financial information. They help owners and managers see the financial position of the business, measure performance and make better decisions.

This dotpoint focuses on three key reports:

- a balance sheet (statement of financial position)

- a profit and loss statement

- a budget

📘 Purpose of financial reports

The overall purpose of financial reports is to help a business understand its financial position and performance. They provide organised financial information that can be used for decision-making, planning and evaluation.

Main purposes for the business

- show the financial position of the business

- measure financial performance over time

- support planning and budgeting

- help managers make better business decisions

- identify financial strengths and problems

- compare actual results with expected results

- provide a formal record of how money was earned, spent and managed

Purpose for different stakeholders

- Shareholders: want to see where their money went and the return on their investment.

- Employees: look for signs of job security and the chance of pay rises.

- Managers: use reports to judge efficiency, set targets and support planning.

- Competitors: may compare financial performance with rival businesses.

- Government: uses accounts to help ensure the correct tax is paid.

- Financiers: banks and lenders use them before approving funds.

- Suppliers: may decide whether trade credit should be offered.

- Potential investors: use them to judge whether an investment looks worthwhile.

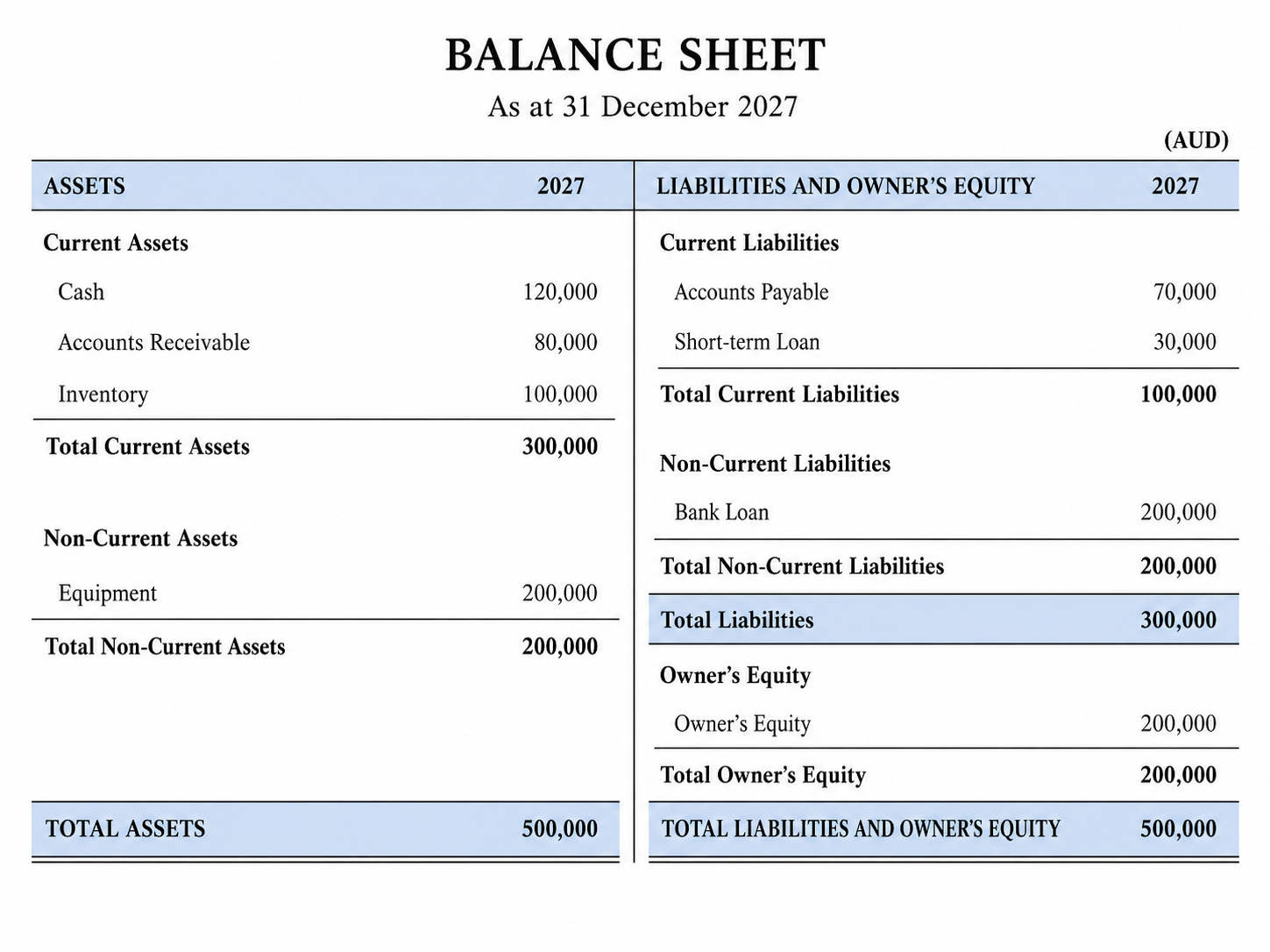

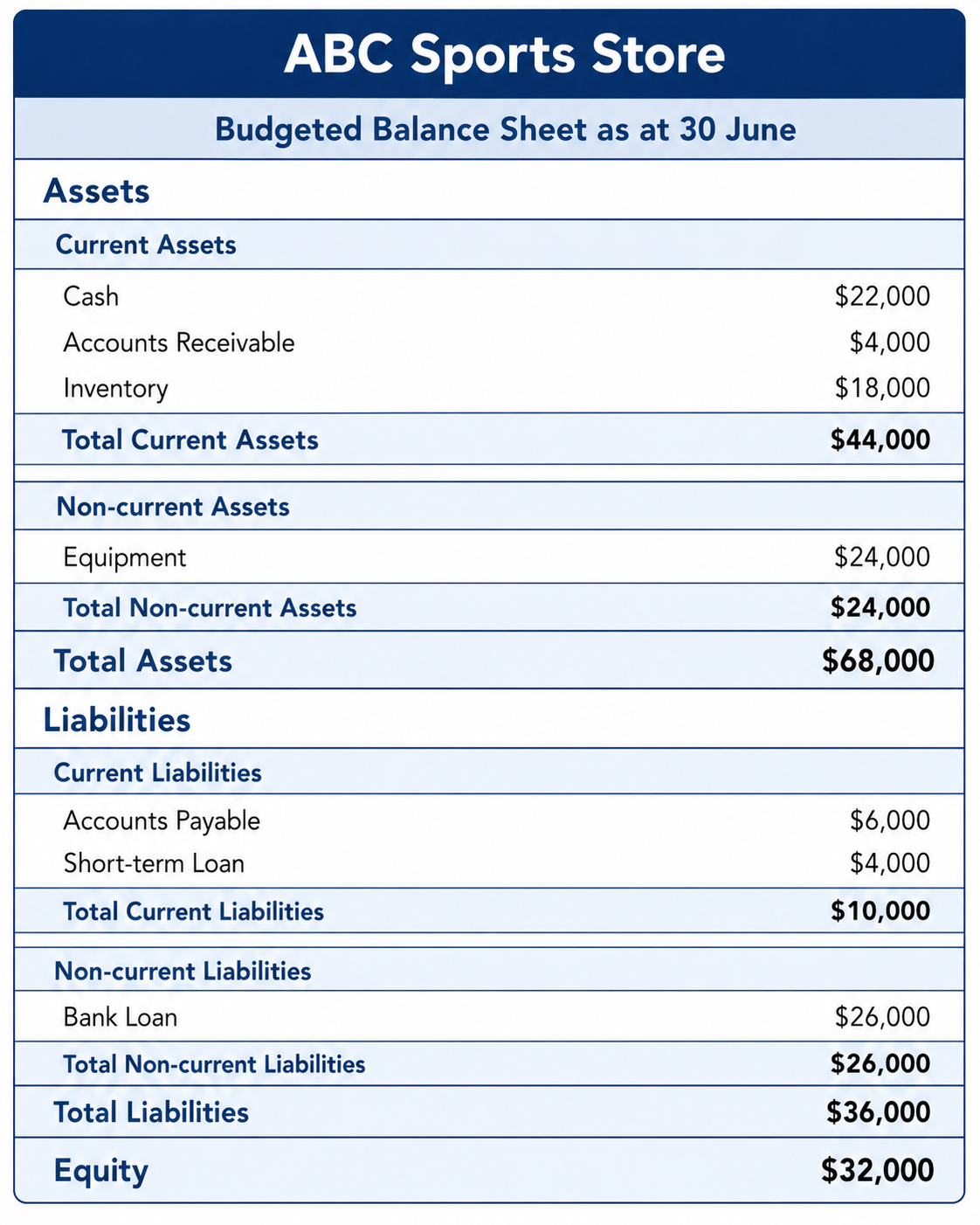

📊 Balance sheet (statement of financial position)

A balance sheet, also called a statement of financial position, shows what a business owns, what it owes, and the owner’s equity at a particular point in time.

Purpose of the report

- shows the financial position of the business on a specific date

- helps owners see whether the business is financially strong or weak

- shows how the business is funded through debt and owner investment

- can help banks, investors and suppliers judge financial stability

- shows whether the business has enough assets to cover what it owes

Features of a Balance Sheet

Assets

Current Assets

Current assets are assets likely to be used, sold or turned into cash within 12 months.

- cash — money in the bank or till

- accounts receivable / debtors — money customers owe the business

- inventory / stock — goods held for sale

- prepaid expenses — payments made in advance

Non-current Assets

Non-current assets are longer-term assets used in the business for more than 12 months.

- equipment

- vehicles

- buildings

- land

- furniture and fittings

Total Assets = Current Assets + Non-current Assets

Liabilities

Current Liabilities

Current liabilities are debts due within 12 months.

- accounts payable / creditors — money the business owes suppliers

- bank overdraft — short-term bank borrowing

- short-term loans

- wages owing

- tax owing

Non-current Liabilities

Non-current liabilities are debts due after more than 12 months.

- bank loans

- mortgages

- long-term finance

Total Liabilities = Current Liabilities + Non-current Liabilities

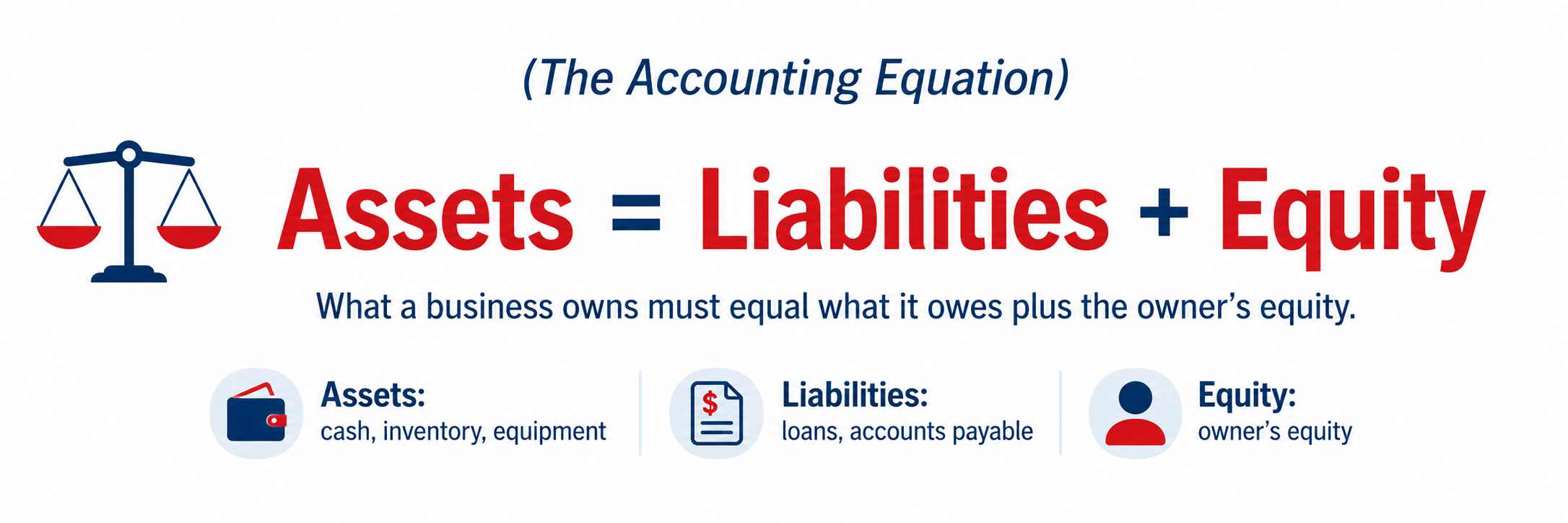

Equity and accounting equation

Equity is the owner’s claim on the business after liabilities are taken away from assets.

The key formula is:

Assets = Liabilities + Equity

Example: if a business has $90,000 in assets and $35,000 in liabilities, equity must be $55,000.

Working capital

Working capital shows whether the business has enough short-term resources to cover short-term obligations.

Formula:

Working Capital = Current Assets − Current Liabilities

If current assets are greater than current liabilities, the business is in a stronger short-term position.

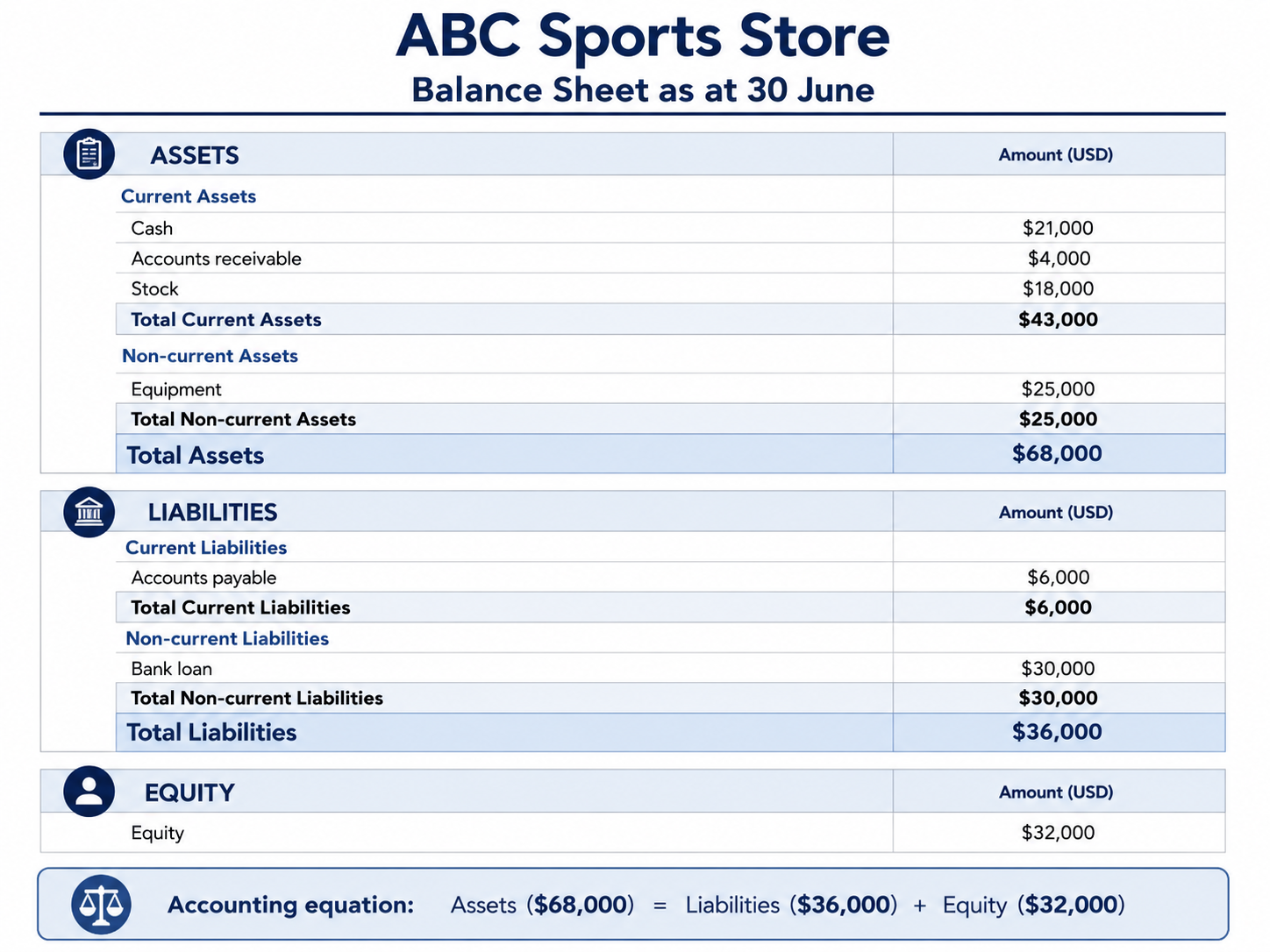

Construction of the Balance Sheet

How to construct a Balance Sheet

Step 1: list all current assets.

Step 2: list all non-current assets.

Step 3: add them together to find total assets.

Step 4: list all current liabilities.

Step 5: list all non-current liabilities.

Step 6: add them together to find total liabilities.

Step 7: calculate equity.

Step 8: check that the accounting equation balances.

See below to see how these transactions are converted into a balance sheet

- the business takes out a $30,000 bank loan

- equipment worth $25,000 is purchased

- stock worth $18,000 is purchased

- the business still owes suppliers $6,000 for some stock purchases

- customers owe the business $4,000 from credit sales

- $21,000 cash remains in the bank

What a balance sheet shows about a business

- financial health — whether the business looks strong overall

- liquidity — whether current assets are enough to cover current liabilities

- stability / solvency — whether the business can manage long-term obligations

- overall value — what the owner’s equity is worth after liabilities are taken away

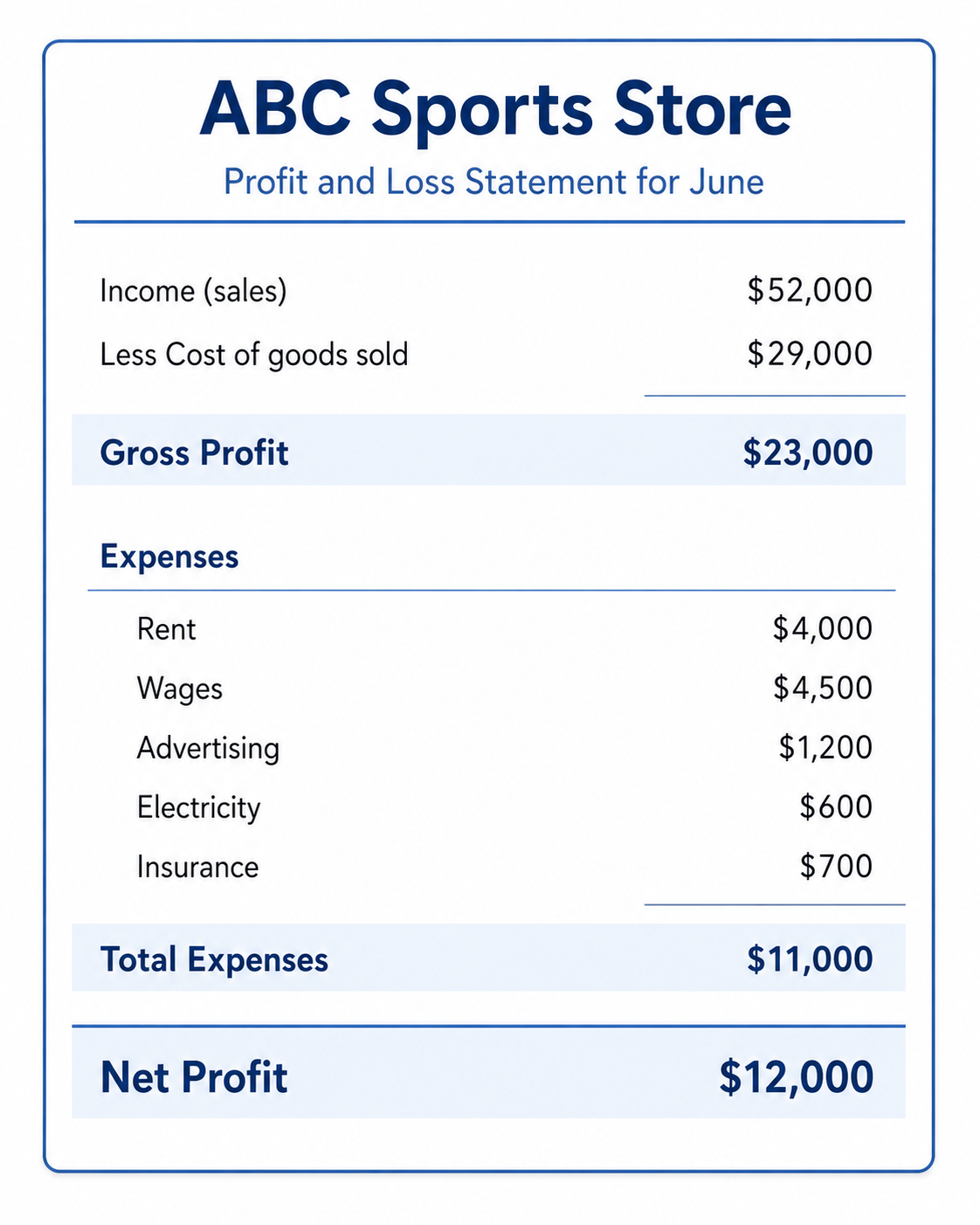

📈 Profit and loss statement

A profit and loss statement shows the income, expenses and final profit or loss of a business over a period of time.

Purpose of the report

- shows whether the business made a profit or a loss over a period

- helps owners judge business performance

- shows whether income is high enough to cover expenses

- can help identify where costs may be too high

- helps managers compare different periods of performance

Features of a Profit and Loss Statement

Income and cost of goods sold

Income is money earned from sales or services.

- sales revenue

- service revenue

Cost of goods sold (COGS) is the direct cost of the goods that were sold.

- purchase cost of stock

- direct freight on stock

- direct materials in a production business

Gross profit

Gross profit is found by subtracting cost of goods sold from income.

Formula:

Gross Profit = Sales − Cost of Goods Sold

Example: if sales are $50,000 and cost of goods sold is $30,000, gross profit is $20,000.

Expenses and net profit

Expenses are the costs of running the business, such as rent, wages, advertising, electricity and insurance.

Net profit is the final profit after all expenses are deducted from gross profit.

Formula:

Net Profit = Gross Profit − Expenses

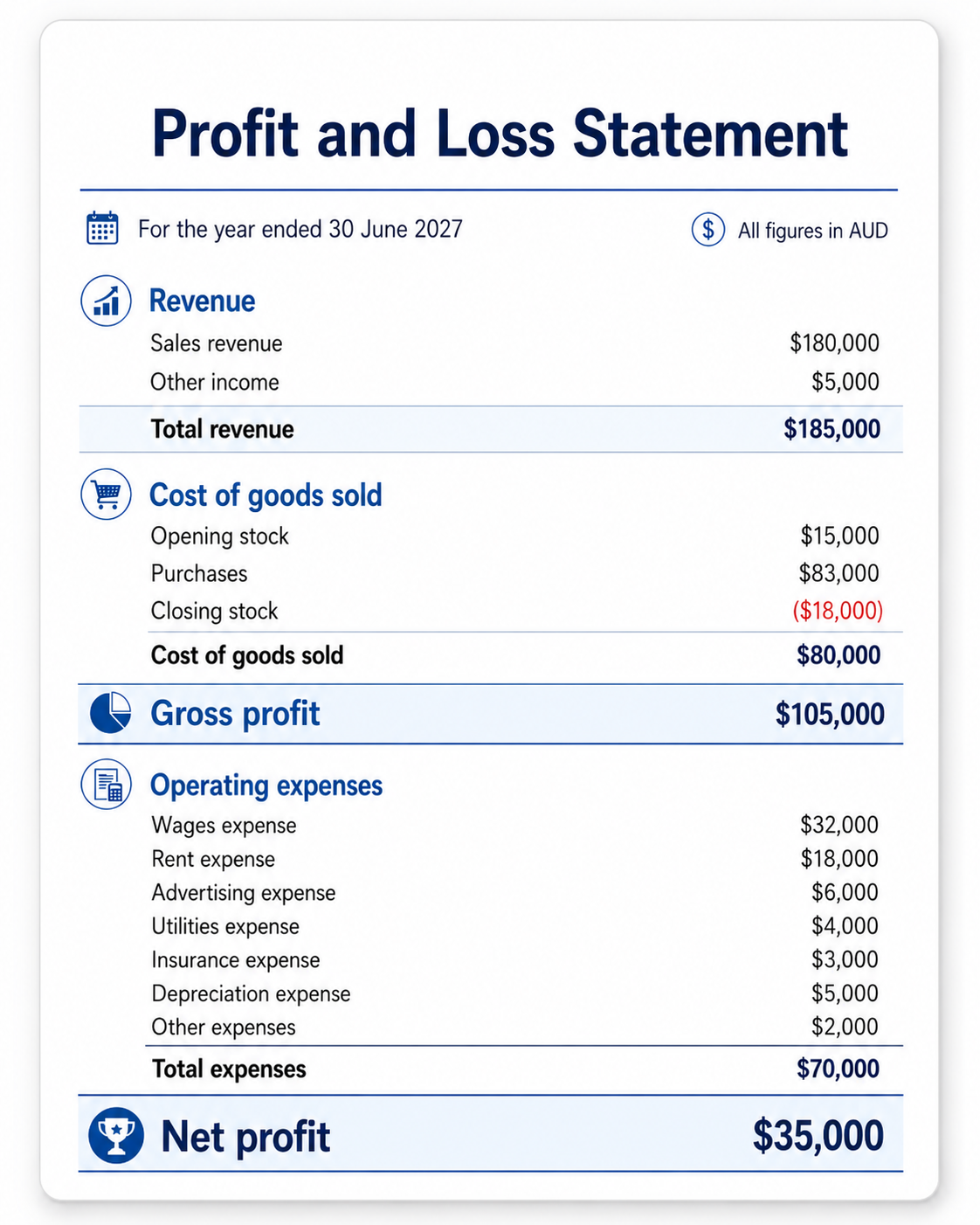

Construction of the Profit and Loss Statement

How to construct a Profit and Loss Statement

Step 1: list all income earned over the period.

Step 2: list the cost of goods sold.

Step 3: subtract cost of goods sold from income to find gross profit.

Step 4: list all operating expenses.

Step 5: subtract total expenses from gross profit.

Step 6: the final figure is net profit or net loss.

See below to see how these transactions are converted into a profit and loss statement

- sales revenue for the month = $52,000

- cost of stock sold = $29,000

- rent paid = $4,000

- wages paid = $4,500

- advertising = $1,200

- electricity = $600

- insurance = $700

What a profit and loss statement shows

- revenue — how much money the business earned

- expenses — how much it cost to run the business

- gross profit — profit left after direct costs of sales are removed

- net profit — final profit after all expenses are removed

- profitability — whether the business is making enough profit from its operations

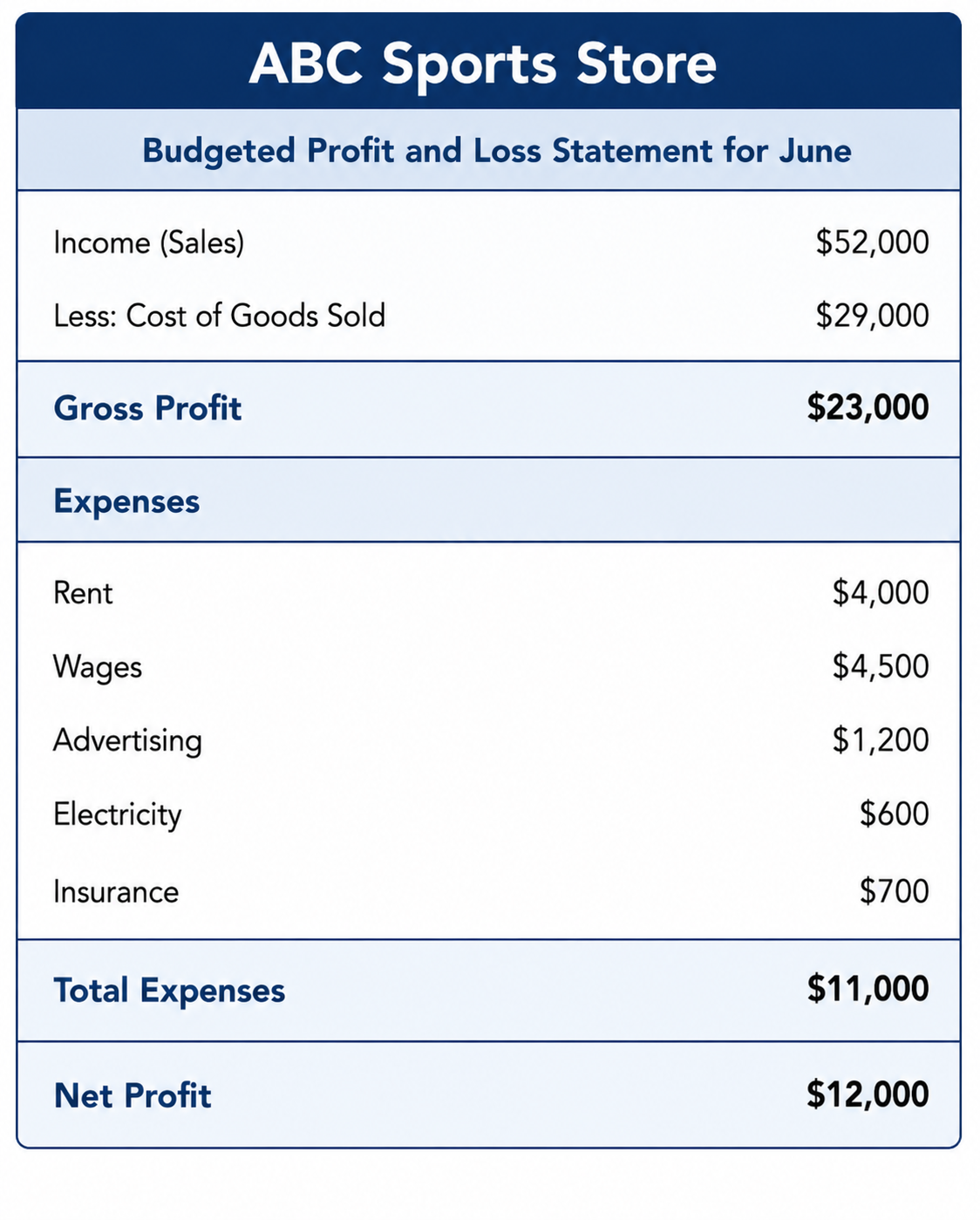

🧾 Budget

A budget is a financial plan for the future. It uses estimates to predict expected income, expenses, cash needs and financial position over an upcoming period.

Purpose of the report

- helps the business plan future income and spending

- supports better control over money

- helps the business avoid overspending

- can be used to compare planned results with actual results later

- helps the business prepare for possible shortfalls

Why estimates matter

Budgets are based on estimates, not exact figures. This means they are useful for planning, but they need to be checked and updated when business conditions change.

That is why a business often compares the budget later with the actual profit and loss statement or other actual financial reports.

Different Types of Budgets

Budgeted profit and loss statement

Definition: a future estimate of sales, cost of goods sold, expenses and expected profit or loss.

Purpose: it is prepared before the actual profit and loss statement so the business can predict performance and set targets.

Budgeted balance sheet

Definition: a future estimate of what the business expects to own, owe and have as equity at a future date.

Purpose: it is prepared before the actual balance sheet so the business can estimate future financial position and structure.

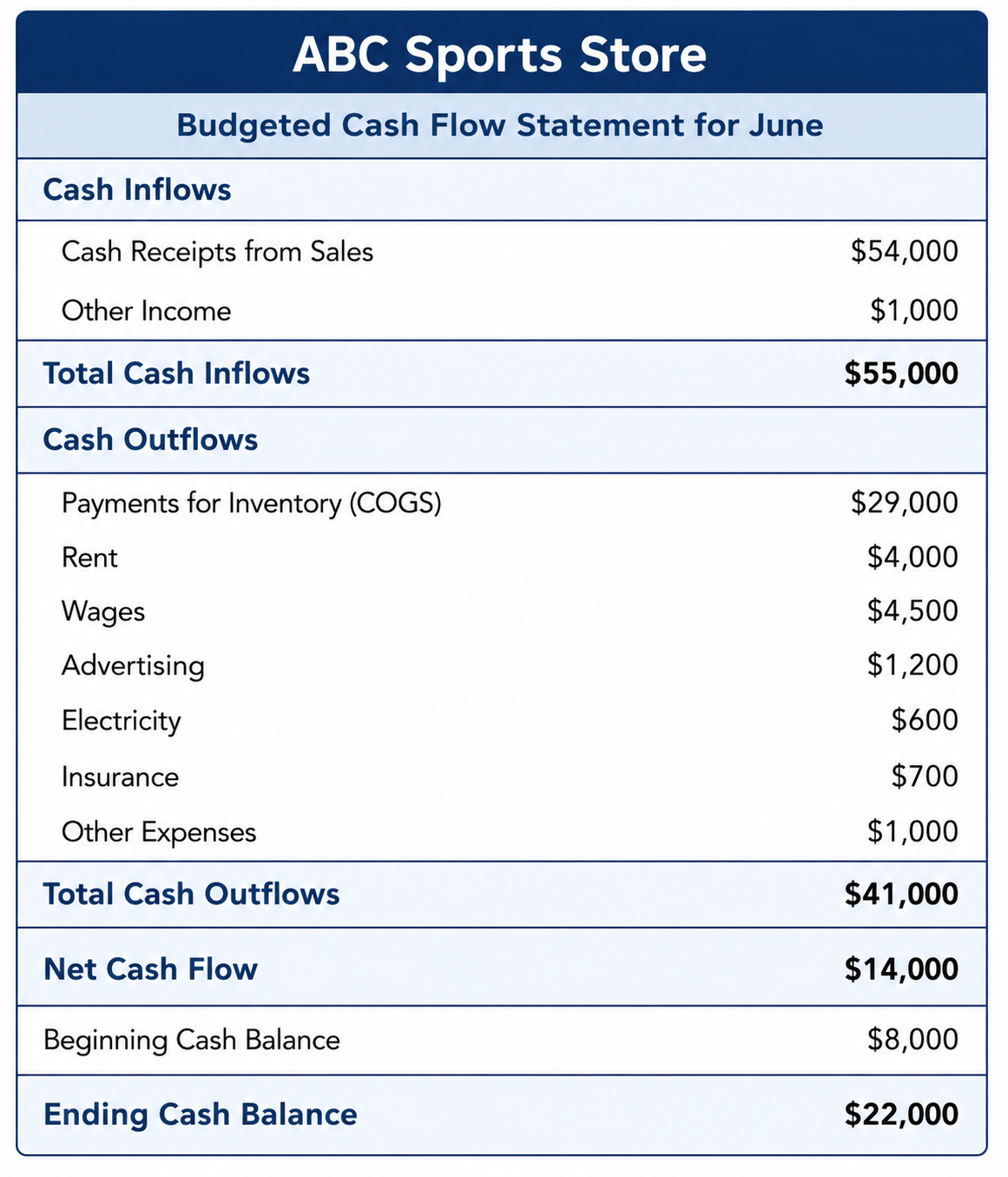

Budgeted cash flow statement

Definition: a future estimate of the cash coming into and going out of the business over a period of time.

Purpose: it is prepared before the actual cash flow statement so the business can predict whether it may run short of cash.

Cash inflows are money coming into the business, such as cash sales, loan receipts or owner contributions.

Cash outflows are money leaving the business, such as wages, rent, stock purchases, loan repayments or electricity bills.

🎧 Prefer listening?

If you prefer listening to the content in podcast format:

🎥 Prefer watching?

If you prefer watching the content in video format:

Biz Fact: A budget predicts the future, a profit and loss statement reveals the truth, and a balance sheet shows how strong the business really is.